Banks Aren't Your Enemy, They're Your Partner in Small Business Funding

Aug 25, 2025

Everyone online has an opinion about banks.

Dave Ramsey says all debt is bad.

Credit hackers teach you to chase points and free flights.

And half of ‘finance gurus’ insist that “credit scores only trap you into paying high interest debt.”

Here’s the truth: if you’re a founder or owner looking for business funding, you don’t get to play by those rules. Avoiding the system doesn’t help you scale. Treating banks like villains doesn’t get you funded.

Approvals come when you start acting like a partner.

Because that’s what banks and small business lenders are looking for: a partner. Not a stranger. Not a risk.

Why the “Banks Are Evil” Story Hurts Borrowers

As individuals, we don’t get to change the system. We can only choose how to react to it.

The idea that “all debt is bad” works if your only goal is to stay out of trouble as a consumer. But if you’re building a business, buying property, or looking for serious business credit lines, you can’t afford to think that way.

Banks aren’t charities. They aren’t predators either. They’re risk managers. They want to put money where it’s most likely to come back (with a profit).

If you want approvals, you have to show up the way a good partner would: reliable, consistent, and worth the investment.

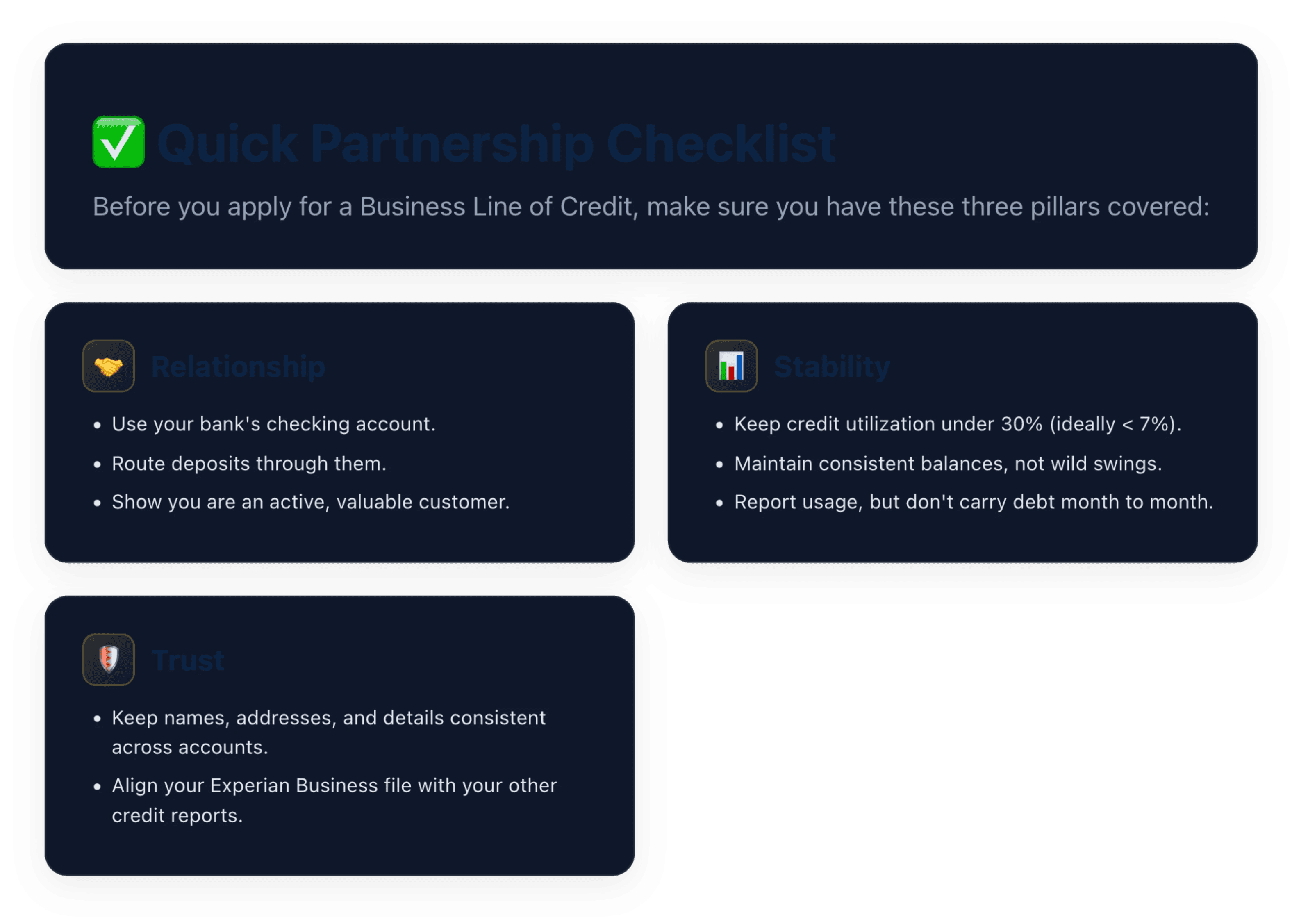

I call it the Partnership Framework. It comes down to three pillars: Relationship, Stability, and Trust.

Pillar 1: Relationship

Banks don’t fund strangers. They fund customers they know.

That means you can’t expect to walk in out of the blue, ask for a six-figure line of credit, and walk out approved. Build the relationship first:

Open their business checking account.

Route your deposits through them.

Use their products (like business credit cards).

It’s no different from any partnership. If you never call, never show up, and never bring value… why would they invest in you?

The stronger your relationship, the more weight your application carries. That’s the foundation of how to build business credit that leads to real approvals.

Pillar 2: Stability

Stability isn’t about being perfect. It’s about being predictable.

Here’s what every small business lender is watching:

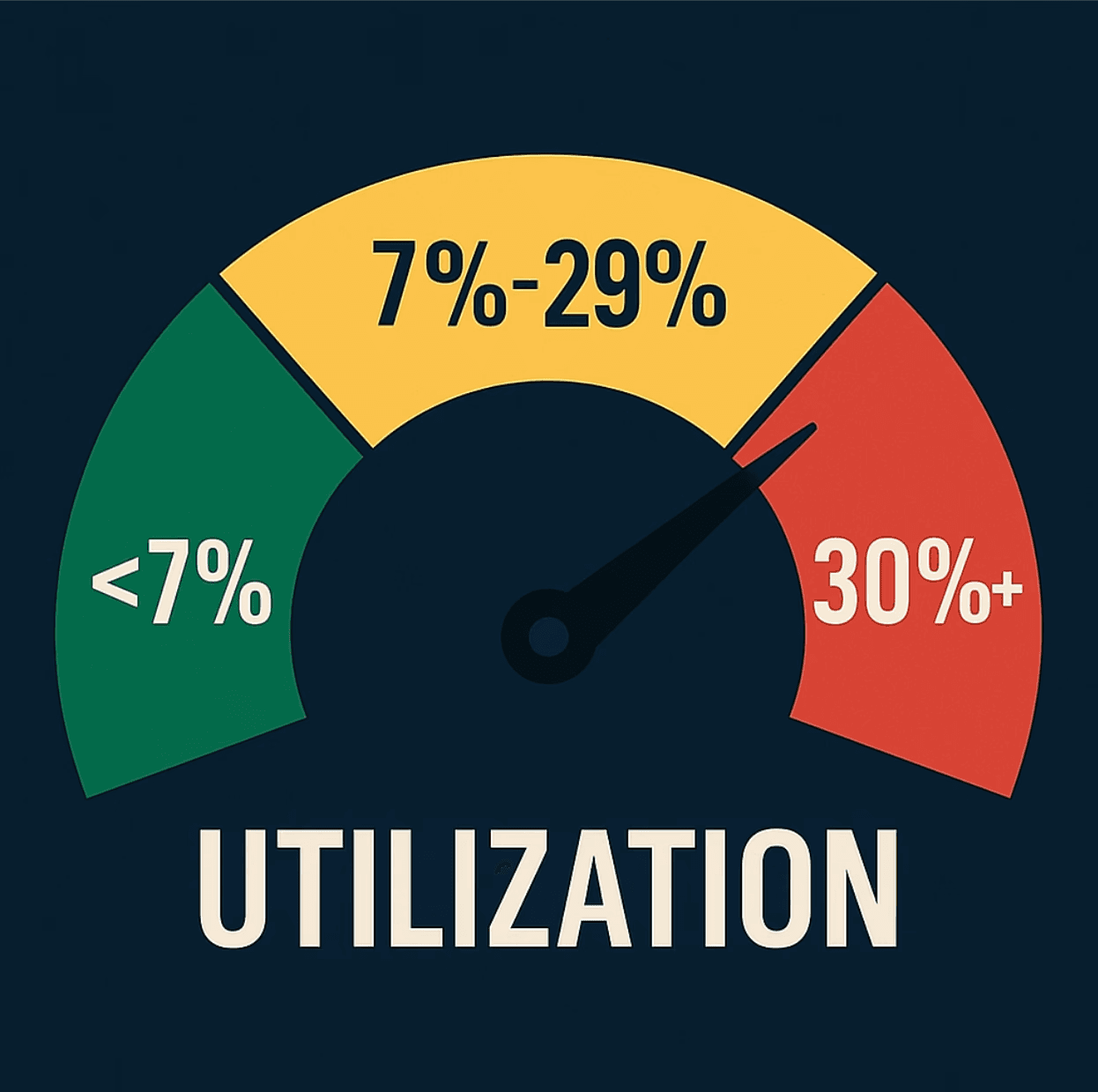

Personal credit card utilization. Anything over 30% is a red flag. Under 7%? You look like a safe bet.

Balances. If your accounts swing from $50K one month to $500 the next, you look volatile.

Payment history. On-time, every time. No excuses.

And here’s a mistake almost everyone makes:

Reporting utilization is not the same as carrying a balance.

Example: You have a $10K limit. You report $2K (20% utilization), then pay it off in full before interest hits. Perfect. You’re showing usage and control.

Different story if you carry that $2K month after month and rack up interest. Now you look like you need the debt to survive. That screams risk.

Think of it like driving a car. Low reported utilization is like having a clean driving record. Carrying debt month-to-month is like living in the car because you’ve got nowhere else to go. One builds confidence. The other looks desperate.

Pillar 3: Trust

Finally, trust. This is where most borrowers get tripped up.

Banks want to know you are who you say you are. That your business is real. That your identity is consistent everywhere they look.

Here’s where small details blow up into big problems:

Your credit accounts show “Jon Smith,” “Jon A. Smith,” and “Jonathan Smith.”

Your business license lists one address, but your bank statement shows another.

Your Experian Business profile doesn’t match your D&B or Equifax Business file.

To you, those might look like harmless variations. To a bank’s underwriting system, they’re red flags. If your story doesn’t match across the board, the system assumes risk.

It’s like online dating: if someone’s name, photos, and social profiles don’t line up, what do you assume? Scam or catfish. Move on.

Banks do the same. Consistency builds confidence. Inconsistency kills approvals.

The Bottom Line

Banks aren’t your enemies. They’re cautious partners.

If you want small business funding, you need to:

Build the relationship.

Show stability.

Prove trust.

You can fight the system, or you can learn to leverage it. Those who choose leverage win every time.

And if you want to make sure you’ve got every box checked before you apply, I’ve put together my full Pre-Approval Checklist. This is the exact process I use with clients to maximize approval odds.

Grab it free here 👉 https://www.skuldhouse.com/fundingblueprint

Book Your Strategy Call

Ready to Secure Better Funding?

Book your strategy call and start your journey.