How to Set Up Your Business the Right Way in 2025 (So You Actually Get Funded)

Aug 11, 2025

Intro: Why “Just Registering an LLC” Isn’t Enough

Most LLCs are dead on arrival with lenders.

If your goal is small business funding, you can’t just register an LLC and call it good.

In 2025, lenders (and the AI tools they use) are looking for consistency, legitimacy, and low risk. That means your business setup needs to be built with fundability in mind from the start.

This guide walks you through how to set up your business the right way, so you’re not just legal. It positions you to build business credit and actually qualify for funding when you need it.

In this guide, you’ll learn how to:

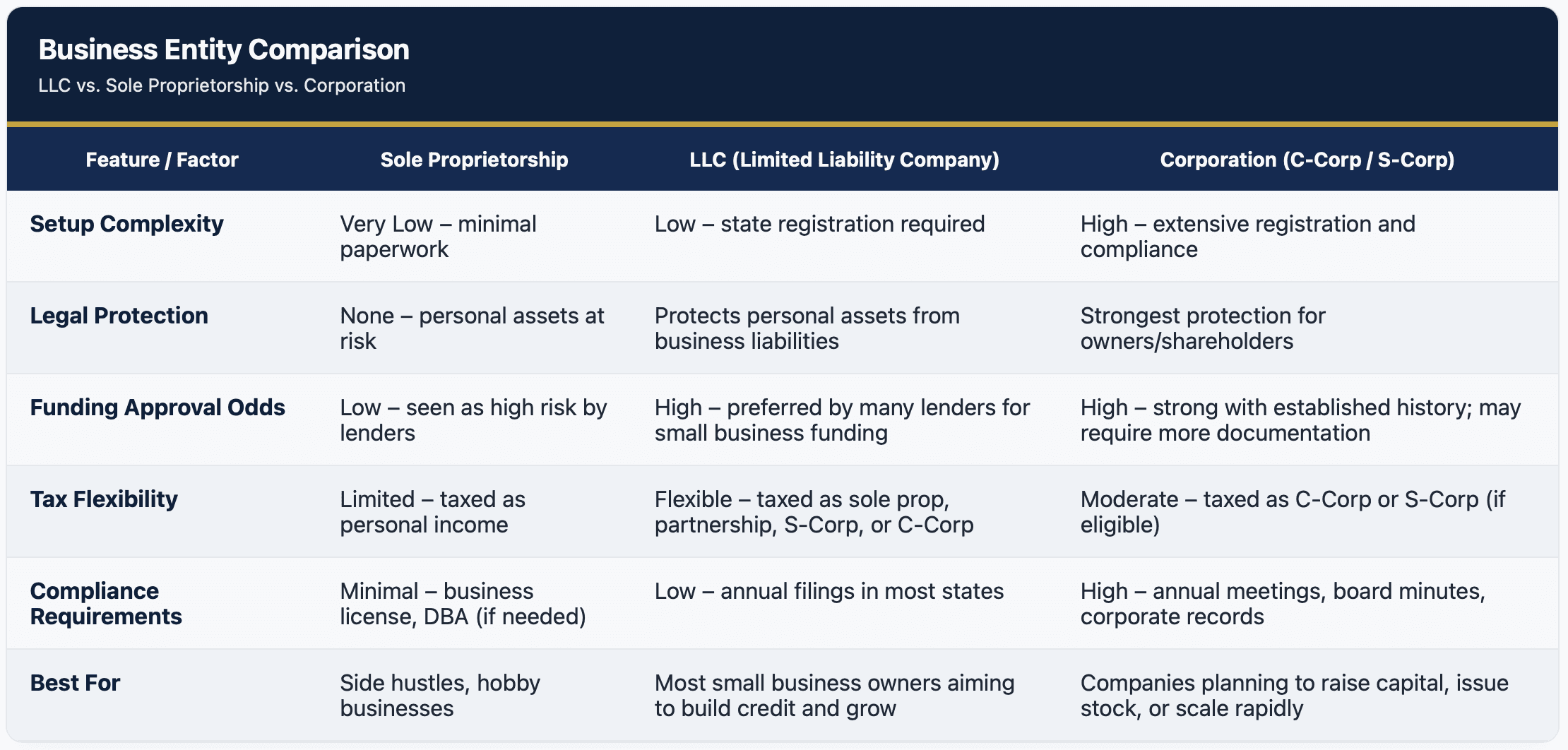

Choose the Right Entity Type

Not all business structures are created equal. This is especially true if your goal is small business funding.

Sole Proprietorships: Simple, but Risky

Sole props are the fastest and easiest to form. No legal paperwork is required beyond a business license (if applicable), and you can operate under your own Social Security number.

But that simplicity comes at a cost:

No separation between you and the business

No liability protection: you’re personally on the hook for debts

Harder to qualify for business credit or funding

Most lenders view sole props as hobby businesses, not scalable operations. If you're serious about building business credit, this structure will hold you back.

Corporations: High Control, High Complexity

Corporations are not to be confused with C-Corps and S-Corps (which are tax designations). Corporations as entities offer the strongest liability protection and a formal structure that’s ideal for:

Startups planning to raise capital or issue stock

Businesses with multiple owners, shareholders, or employees

Entrepreneurs who want a clean, scalable structure from day one

However, they come with more compliance requirements, tax complexity, and administrative upkeep.

LLCs: The Best Middle Ground

LLCs (Limited Liability Companies) strike a strong balance:

Personal liability protection for the owner(s)

Less paperwork and fewer compliance burdens than a corporation

Flexibility to be taxed as a sole prop, partnership, or even an S-Corp

Most small business owners (especially those focused on qualifying for small business funding) choose an LLC because it offers the credibility and structure lenders want, without the overhead of a corporation.

✅ Pro tip: You can always restructure later. But if you’re starting from scratch, an LLC is usually the best launchpad for building credit, protecting yourself legally, and setting up your business to scale.

Choose a Strategic Name and NAICS Code

Your business name and NAICS code may seem like boring paperwork. However, in 2025, they’re two of the most important signals lenders use to assess risk. They work together to define your industry, expected operations, and credibility.

Start With a Name That Doesn’t Get Auto-Flagged

Most business owners choose a name that sounds professional. But risk engines don’t think like customers. Words like:

“Investments”

“Credit Repair”

“Real Estate”

“Capital” or “Holdings”

…can raise immediate red flags with underwriters and AI models.

Even worse? A name that conflicts with your NAICS code.

Example: “Premier Logistics LLC” registered under a consulting code will look like fraud to most banks.

✅ Keep it simple and fundable: Neutral, broad names that match your actual operations (or the story you’re telling with your NAICS) are best.

Then, Choose a Lender-Friendly NAICS Code

Your NAICS code (North American Industry Classification System) is the official industry tag for your business. It shows up in public databases, LexisNexis reports, and lender risk models even if you don’t enter it on an application.

Some NAICS codes are known approval killers.

Others, like 541611 (General Management Consulting), are considered low-risk and fundable.

These 541-series consulting codes are ideal if:

You offer advisory or service-based work

You’re positioning for B2B relationships

You want to maximize fundability across industries

Advanced Strategy: Structuring a Funding Entity

In some cases, entrepreneurs separate their operations into multiple entities:

A fundable consulting entity built around a 541 code

and

One or more operating companies with higher-risk NAICS codes

The fundable entity secures capital, then lends it internally to the others.

This strategy can:

Protect assets

Improve approval odds

Unlock higher limits at better rates

⚠️ Important: This structure is complex and requires legal/tax guidance. It’s not a DIY move. It is worth understanding if you plan to scale multiple entities, though.

I’ll be writing more about how I use this strategy in my own business (and with advanced clients) in a future post.

Use a Real, Verifiable Business Address

“Just get a virtual address” is some of the worst advice in the business credit world. And it is EVERYWHERE online.

In 2025, banks and lenders are tightening their standards. They want to verify that your business actually operates at a physical location. They’re using databases, AI models, and fraud detection systems to do so.

What Doesn’t Work Anymore:

Mail-forwarding services like iPostal1, Earth Class Mail, or UPS Store addresses

PO Boxes (even the ones disguised as street addresses)

Locations that appear in high volumes across business applications

These types of addresses often appear in fraud cases, can’t be verified by underwriters, and don’t pass the “real business presence” test. Some banks, including Wells Fargo, now reject them outright for account openings.

What Does Work:

Address Type | Fundability | Notes |

|---|---|---|

Commercial office | ✅ Strong | Most credible. Signage or a lease in business name = trustworthy |

Coworking space | ✅ Good | Credible if staffed and verifiable |

Home address | 🟡 Acceptable | Works if consistent, but may raise privacy or compliance issues |

Mail-forwarding service | ❌ Risky | Often flagged as non-legit or associated with past fraud |

💬 Some people worry that co-working spaces like Kiln or WeWork are problematic because multiple businesses share the same suite number. In practice, these are often more fundable than a home address: as long as the space is staffed, and verifiable.

Why Consistency Matters More Than Perfection

🧪 Real example: I was approved for a business line of credit using my home address.

That was only possible because I did everything in my power to look legitimate and trustworthy everywhere else.

My state registration, EIN, business bank account, and license filings all matched exactly. That’s what lenders look for: a borrower profile that feels complete and low-risk.

Pro Tip:

If you're starting lean, a home address can work. Just make sure:

It’s legal to operate from there in your state or city

You use it consistently across all business records

You’re not mixing personal and business finances

As your business grows, consider transitioning to a staffed coworking space or commercial lease to improve fundability and protect your privacy.

Get Your EIN (Correctly)

Your Employer Identification Number (EIN) is like a Social Security number for your business. It’s used to open business bank accounts, apply for credit, and verify your identity across federal and commercial databases.

But here’s what most people don’t realize: lenders don’t just check whether you have an EIN. They cross-reference it against your entire business profile.

What Can Go Wrong

If your EIN data doesn’t match your:

Legal business name

Registered address

Business structure

NAICS code (selected or inferred)

…you introduce risk signals into systems like LexisNexis, Dun & Bradstreet, and Early Warning Services. Those mismatches can trigger identity verification failures or get your application kicked to manual review or worse, denial.

⚠️ Important: Many lenders pull EIN info directly from IRS records or 3rd-party sources. If something’s off, you may not even realize why you’re being flagged.

How to Do It Right

Apply directly through the IRS website (never pay for this)

Use the exact business name you registered with your state, including punctuation and capitalization

Match your business address and structure precisely

If asked for your industry, choose your pre-selected NAICS code to keep everything aligned

💡 Pro tip: Take 30 seconds to copy/paste your business name and address from your state registration into the IRS form to avoid typos. Precision matters.

Why This Step Matters for Fundability

Your EIN is one of the core data points used to create your “borrower identity” across databases. If it doesn’t match your other filings, you’re already starting with friction in the funding process.

Create an Operating Agreement (Even if No One Asks Yet)

You might not be legally required to create an operating agreement when forming a single-member LLC, but if you skip it, it can still come back to bite you.

Lenders, banks, and even some vendors will sometimes ask for it as part of their due diligence. It’s one of the few internal documents that shows you’re running a real business, not just holding an EIN and hoping for funding.

My Mistake: I Got Lazy

I already had an operating agreement for my main business. When I opened my first business checking account, no one asked for it. So, this time around, I didn’t bother.

When the banker asked if I had one, I froze.

I knew exactly what it was, but I hadn’t created one yet.

So, I opened my laptop and drafted it right there in the lobby. Took five minutes. But, if I hadn’t known what to include, it could’ve stalled the entire process.

What an Operating Agreement Does

Establishes ownership and control of the business

Details how profits, losses, and responsibilities are managed

Adds legitimacy even if you’re the only member

It’s also often required when:

Opening certain types of bank accounts

Applying for larger lines of credit

Getting reviewed by underwriters for risk scoring

Bottom Line:

Don’t wait until someone asks. Draft one early, keep it on file, and update it if your ownership or structure changes. It’s a small detail that adds a big layer of trust to your borrower profile.

Understand AI Risk and Borrower Identity

It’s easy to think lenders are just looking at your credit score and LLC paperwork. But in 2025, that’s not how funding decisions are made.

Lenders (especially banks and fintechs) are using AI models, identity graphs, and behavioral pattern-matching tools to assess whether your business profile looks credible, consistent, and low-risk.

And that means your borrower identity matters more than ever.

What Is Borrower Identity?

It’s the collection of data points that underwriters and risk models use to determine whether your business is real, trustworthy, and fundable. This includes:

Your business name, structure, and NAICS code

Your EIN and associated IRS records

Your address (and whether it appears in flagged databases)

Your phone number and email domain

Your LexisNexis and SBFE profile data

Your banking relationships and login behaviors

⚠️ If any of these details are inconsistent or mismatched even slightly, it can flag you as high risk before a human ever sees your application.

My Own Experience: Even a Clean Profile Gets Flagged

I walked into my credit union to open a business checking account.

Everything was legit: real business, clean profile, matching documents.

But their AI-based identity tool falsely linked me to someone else… a felon in Florida.

I wasn’t denied, but I had to re-verify every single detail:

Full legal name

Date of birth

Address

Business documents

It added unnecessary friction to a process that should’ve been simple.

The Lesson? Consistency Beats Perfection

It’s not just about having an EIN or an LLC. It’s about how all your data fits together.

If your bank account lists one address, your IRS records list another, and your D&B file is half-complete, you’re going to hit resistance.

That’s why the next step isn’t just admin.

It’s one of the first ways to anchor your borrower identity in real-world activity.

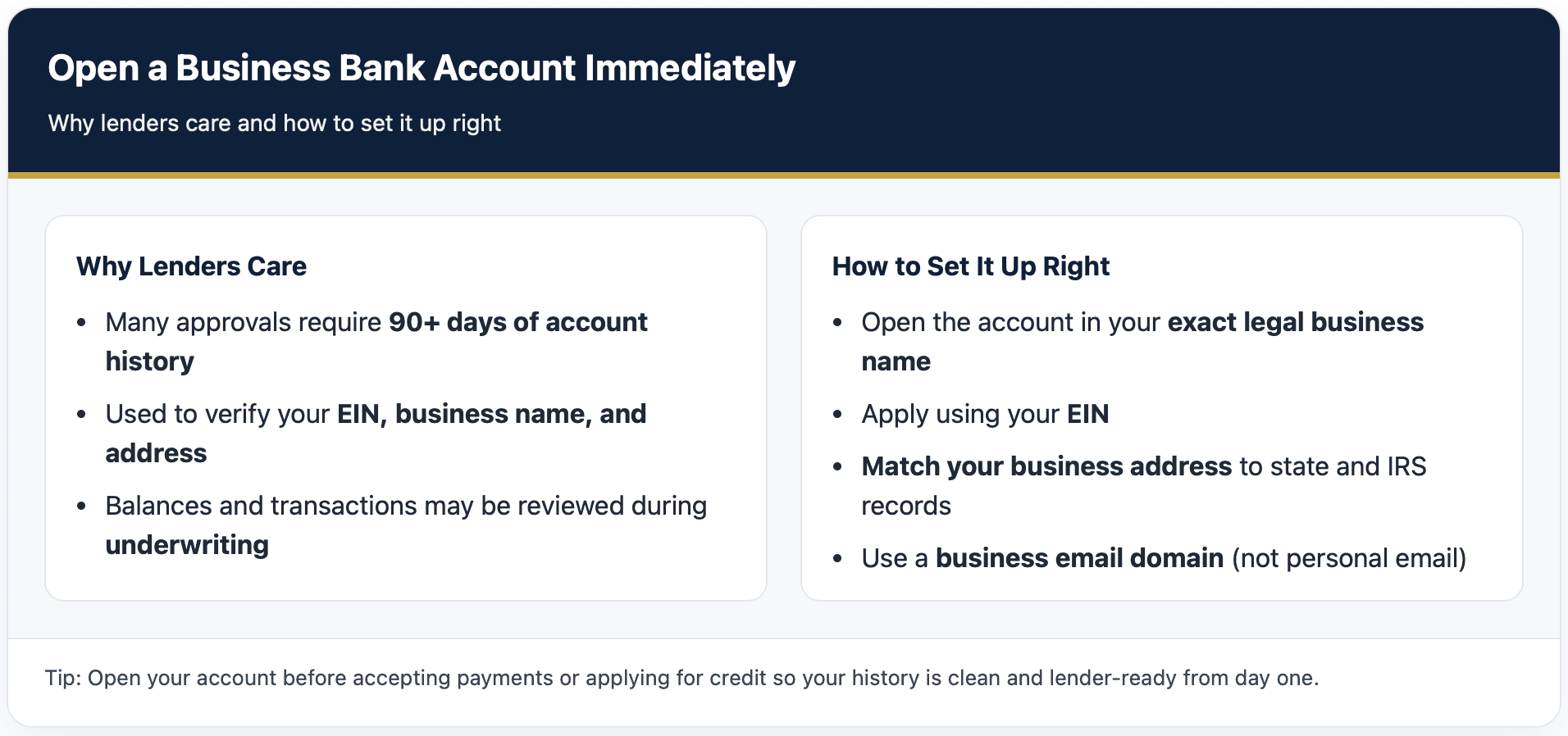

Open a Business Bank Account Immediately

Once your business details are locked in and consistent, the next step is to anchor your borrower identity with a real, active banking relationship.

To lenders, your business bank account is more than a place to store money. It’s a live proof point that:

Your business exists

It operates separately from your personal finances

It can handle funding responsibly

Why This Step Matters for Funding

Many lenders require 90+ days of account history before approving credit

The account details (name, EIN, address) must match your IRS and state filings for maximum credibility

Underwriters may review average daily balances, deposit activity, and transaction history during manual review

If you’re commingling funds or skipping a dedicated account, you’re undermining the credibility you just worked to build.

How to Set It Up Right

Open the account in your legal business name, exactly as filed

Use your business EIN (not your SSN)

Match your business address to your registration and IRS records

Use a business email domain (not Gmail, Yahoo, etc.) for the bank’s contact info

⚠️ Even a minor mismatch between your bank account and your IRS filing can create risk flags in systems like LexisNexis and Early Warning Services.

Pro Tip: Timing Matters

Open your account before:

Accepting your first payment

Paying vendors

Applying for credit

That way, every transaction contributes to a clean, lender-ready history from day one.

Next Steps: From Setup to Funding

Getting your business structure right is only step one.

If your goal is small business funding, the next step is to start building your business credit profile and banking relationships.

Check out this guide here: How to Build Business Credit in 2025

If you aren't sure business funding is your next step, check out our Borrower Type Quiz. It evaluates your credit profile, funding goals, and borrower positioning.

Test your funding readiness and stop guessing at your credit strategy.

Book Your Strategy Call

Ready to Secure Better Funding?

Book your strategy call and start your journey.